Sex sells – Grindr (GRND.NYSE)

The adage “sex sells” couldn’t be more fitting for a recent addition to the portfolio – Grindr (GRND.NYSE), the world’s dominant gay ‘hookup’ app. Due to some fundamental differences between the gay male community and the heterosexual community, GRND benefits from some incredible network dynamics that place it among the best businesses in the world. It’s night and day between GRND and its heterosexual dating app peers, Match Group (MTCH.NAS) and Bumble (BMBL.NAS).

Similar to how we view Airbnb (ABNB.NAS) and Booking Holdings (BKNG.NAS) as royalties on global travel spend, we believe GRND is effectively a royalty on gay sex – and boy is business booming…

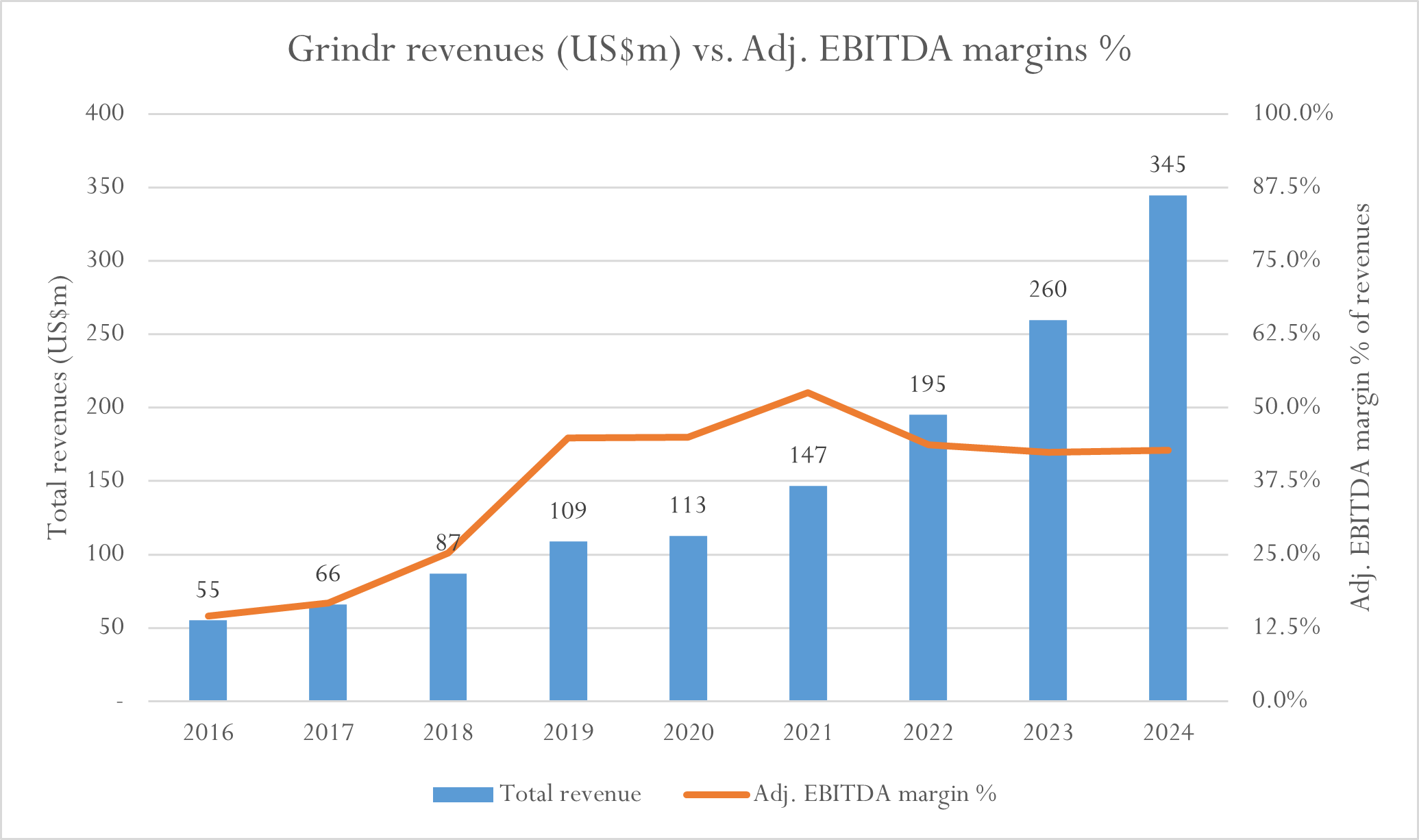

Since 2017, revenues have grown more than fivefold, compounding at +26.6%, while Grindr’s user base expanded at a more modest +8.9% p.a. without material marketing investments.

Source: GRND SEC filings

Most importantly, this impressive growth has required little by way of incremental capital investments into the business, with the business having been bootstrapped and funded by reinvested profits from inception. Over the last 4 years, GRND’s free cash flows before interest and tax (FCFBIT) – an important measure of profitability – averaged ~37.9% of revenues, as opposed to MTCH’s 29.8% and BMBL’s 21.9%.

This fountain of cash was produced with a very lean team. In fact, at one point under its Chinese ownership, Grindr had virtually no employees at all, yet their business kept growing! Including third party contractors, GRND had only ~160 employees through 2024, equating to FCFBIT per employee of ~$830k, above Airbnb’s (ABNB.NAS) ~$675k per employee

So, what’s driving and protecting this mouthwatering profitability?

The answer lies in its unique and powerful network dynamics. Like many other social applications, marketplaces, and other internet-based software companies, GRND benefits from network effects such that growth in its user base increases value to other users on the network, improving the overall user experience whilst making it more difficult to compete with.

Unlike heterosexual dating apps, Grindr caters to an audience primarily seeking casual, immediate connections – more akin to an Uber Eats for sex than a conventional matchmaking platform. Your Portfolio Manager can personally attest to the fundamentally different experience on Grindr compared to heterosexual dating apps Hinge, Tinder, et al… we’re yet to find a limit of the things we’re willing to do to uncover unique insights and investment opportunities!

This creates an inherently high-engagement network where user churn is minimal. Additionally, men-who-have-sex-with-men (MSMs) tend to have far more sexual partners over their lifetime (67 on average by age 35-39 vs. 12 for heterosexual men), with many engaging in open relationships, ensuring they remain active on the platform far longer than their heterosexual counterparts[1].

Beyond sheer engagement, Grindr’s network benefits from powerful reinforcing factors. Nearly 30% of weekly active users (WAUs) are traveling at any given time, making the network’s value extend well beyond a single city, unlike hetero dating apps where users overwhelmingly seek local matches[2]. Age cohort cross-over is also far more prevalent among MSMs, making the network more resilient to shifting generational preferences. Last, but certainly not least, 30% of Grindr’s users are discreet or closeted, meaning there are virtually no alternatives that provide the same level of anonymity for casual encounters[3].

Ultimately, Grindr’s atomic network – the minimum network size needed for it to be useful and self-reinforcing – is far larger than that of hetero-focused dating apps like Tinder or Hinge, making the barriers to entry in MSM ‘dating’ apps prohibitively high. Because the size of the network itself is the primary value driver rather than the sophistication of their matchmaking algorithms, Grindr’s large user base, now over 14.7 million monthly active users (MAUs), comprises its impenetrable moat.

The relative strength in Grindr’s network effects vs. heterosexual dating apps is evident in the fact they’ve spent, and continue to spend, virtually nothing on marketing to attract their ever-increasing user base which grows primarily through word of mouth amongst the MSM community. Over the last four years, GRND spent an average of 1.6% of revenues on advertising while users grew at high-single digit rates annually vs. MTCH and BMBL whose user bases grew more modestly despite spending 15.8% and 21.9% of revenues, respectively, on customer acquisition. GRND is the connective tissue of the MSM community, serving a crucial role connecting a highly engaged user base with very few alternatives, vs. Tinder, Hinge, and Bumble who compete against many alternatives for heterosexual males and females to find long-term partners.

Attempts to compete with Grindr have repeatedly failed. Even its own founder, Joel Simkhai, struggled to gain traction with his competitor, FindMotto, which shut down in 2024. Other challengers, like Archer (MTCH’s LGBTQ dating app), have similarly fizzled out. As we said in our Airbnb post, network effects are like gravity: the largest network will (most likely) continue to be the largest network.

Despite its dominance, Grindr has barely scratched the surface in monetizing its user base. Historically, its product has remained largely unchanged since inception, but with new management clearing technical debt, several monetization opportunities are now coming to fruition.

Grindr’s advertising revenue per free user grew +46% in 2024 to $0.34 per month, yet we still believe the business is in its infancy. Cost per thousand impressions (CPMs), a common metric used to measure performance of marketing spend, remain well below their potential for multiple reasons. To date, most of their in-app advertisements have come from third-party ad networks such as AppLovin, Google AdMob, etc., which provide app developers with high-volume, low CPM ad inventory from predominantly mobile gaming advertisers (i.e. Candy Crush). These ads typically have little relevance to Grindr users, add friction to the user experience, and carry a high cost associated with sourcing inventory from the third-party ad network.

The reality is that GRND has a highly affluent user base which simultaneously happens to be a very difficult demographic to target on other advertising platforms. For instance, META recently removed the ability for advertisers to target by sexual orientation in response to the European Unions concerns around user privacy, leaving many a LGBTQ-focused marketing teams high and dry[4]. Despite this, GRND’s average advertising monetisation rates significantly trail the likes of Meta (META.NAS), Snap Inc. (SNAP.NYSE), and Pinterest (PINS.NAS) – see below.

Sources: META, SNAP, PINS, GRND public filings

As GRND adds more direct partnerships with brands selling products more aligned with the MSM community and continues to invest in targeting and attribution tools on their platform, we expect to see CPMs and average revenues per free user to lift materially above current levels.

Similar to their advertising business, GRND’s core functionality had been significantly under-invested in for many years, especially when compared to the hetero dating apps, Tinder and Hinge. This changed very recently with the release of several new features aimed at better catering to GRND’s core hookups use case (“Right Now”), making a user’s profile visible to more users in their area (“Boosts”), and changing your location ahead of travel (“Roam”). These features are in various stages of their broader rollout and potential monetisation, however early tests show promising results that they will provide significant value to Grindr users.

There are many other levers GRND can pull to increase both Paying Users (currently 7.7% vs. Tinder’s ~21.3%[5]) and Average Revenue per Paying User (ARPPU), including further merchandising, pay-wall optimisation and other upcoming features that haven’t been mentioned, however, we’re most excited about their upcoming Relationships initiatives. Grindr’s usage has historically oriented around casual hookups, though there is a growing portion of their user base that are looking for a long-term partner. Grindr has done little to cater for this intent, leading to frustrating experiences for this segment of users who have consequently turned to Tinder and Hinge for their recommendation algorithms and rich profiles on users with more ‘serious’ intentions.

To that end, the company is set to launch a ‘Discover’ tab in the Grindr app this year that will leverage investments in machine learning to present users with people they may find interesting all around the world. While there is significant uncertainty around this potential new product, we believe there is one fundamental reason why, if successful, we think this will significantly increase both payer penetration and monetisation per user above their hetero-focused dating apps counterparts MTCH and BMBL – there is generally a low geographic density of MSMs, making it far less likely that “the one” that you end up settling down with is in your area, that you’ll bump into randomly on the street, or meet through Grindr’s existing user experience. It’s for this reason that many gay men will travel to find a long-term partner. Through investing in recommendation capabilities that display potential matches in other cities and even countries, Grindr could easily serve as a relatively inexpensive alternative to find a long-term relationship, re-engage users lost to other apps and improve user monetisation rates over the longer-term. We will be monitoring this development closely as we view it as the largest profit opportunity for the business over the medium-term. Pleasingly, the company already has the most important asset required to make this emerging feature a success – the largest network of potential matches.

Outside of investing in their advertising business and other new features, Grindr still has a large opportunity left to continue growing its user base. We estimate that Grindr’s market penetration of their ex-China international market opportunity is ~13%, significantly below their ~41% market penetration in their core US market. The company is now beginning to localize its app for key underpenetrated markets such as Brazil, Spain, the Philippines, and India, as well as investing in brand awareness campaigns through partnerships with local influencers and targeted advertising spend, which we expect to drive growth in international MAUs and Paying Users for many years to come.

Between these three major strategic initiatives – improving their advertising business, adding new monetizable features, and international expansion – we believe GRND will be able to comfortably surpass their 2024 Investor Day revenue growth targets of 23% p.a. over the medium term. Given the operating leverage inherent in the business, we expect this topline growth to translate to some impressive growth in free cash flows, of which, a large portion will be returned to shareholders in the form of share repurchases as financial leverage returns to more conservative levels.

In summary, we believe GRND is still in the early innings of its monetization story with its best years still ahead. For the patient investor, Grindr represents an asymmetric opportunity in a business with unparalleled economics. While ~41x free cash flows looks like an expensive price to be paying, the significant growth in free cash flows per share that we expect the company to achieve over the next 5-10 years should see us earn an attractive rate of return on our investment in the business.

BM.

This document contains general information only and is not an investment recommendation. Blue Stamp Company Pty Ltd (ACN 141 440 931) (AFSL 495417) (‘Blue Stamp’) is the Trustee and Manager of the Blue Stamp Trust (‘Trust’). Blue Stamp accepts no liability for any inaccurate, incomplete or omitted information of any kind or any losses caused by using this information. Blue Stamp does not guarantee the performance or repayment of capital from the Trust. Past performance is not a reliable indicator of future performance. Please consider the Information Memorandum (‘IM’) and investment risks before making any decision to invest, acquire or continue to hold units in the Trust.

[1] Source: NLM: A comparison of sexual behaviour patterns among men who have sex with men and heterosexual men and women

[2] Source: Grindr (GRND.NYSE) Q4’24 Shareholder Letter

[3] Source: Bloomberg TV: Grindr CEO on protecting user safety globally

[4] Source: BBC – Meta must limit data for personalised ads – EU court

[5] Source: Match Group (MTCH.NAS) 2024 Investor Day