Royalties in the global travel industry – Airbnb (ABNB.NAS)

The online travel agency (OTA) or ‘intermediary’ industry contains some of the highest quality businesses we’ve come across, including Airbnb (ABNB.NAS) and Booking Holdings (BKNG.NAS), whose revenue streams we view as royalties on global travel spend. After many years of consolidation since the industry’s inception in the early 90’s, significant amounts of hotel and other short-term accommodation bookings are now completed through the largest global OTAs, with the previous leader Expedia (EXPE.NAS) now in second place behind BKNG – and ABNB hot on its heels. ABNB and BKNG are two fantastic businesses that earn a commission of ~13-15% of gross booking value (GBV) made through their platforms.

Both Airbnb and Booking.com enjoy high margins and profitability because many guests, and in Airbnb's case, accommodation suppliers, come directly to their platforms due to the wide range of accommodations and strong brand presence. Over the last 5 years (including 2020 which saw annual GBV down over -37% and -63% for ABNB and BKNG respectively), ABNB and BKNG have produced free cash flows (FCFs) equating to 3.8% and 3.5% of GBV respectively, with recent FCFs much higher than the average as a percentage of GBV.

Impressively, this incredible profitability is produced with very little capital investment, allowing both ABNB and BKNG to grow at very high rates while returning nearly all cash generated back to shareholders in the form of share buy-backs and dividends. On a combined basis, ~$36.1 billion in both equity and debt has been invested cumulatively since business inception to date, producing a combined ~$9.87 billion in free cash flows in 2023, equating to a return on total capital invested of ~27.4% p.a (with incremental returns on invested capital being much, much higher). They’re the kind of businesses that we dream about!! It’s hard to overstate just how rare these returns are. Most businesses over long periods of time will fail to produce meaningful amounts in cash compared to the capital that has been invested in them.

The capital light nature of the dominant OTAs is underpinned by the ‘float’ that they benefit from, whereby they receive payments up front from guests booking accommodation through their platform. These payments (or guest deposits) are only released to the host or accommodation supplier after check-in, which often occurs many months after booking. This compares to payment facilitator (“payfacs”) businesses like Square, Stripe, Adyen, Tyro, and many others, who, to remain competitive in the market, often pay out funds to sellers before the payment settles – requiring a constant injection of capital to support growth.

While they’re capital light by nature, both ABNB and BKNG’s largest assets (which don’t show up on the balance sheet), and the primary source of their wide economic moats, are their immense two-sided networks of both accommodation suppliers and guests. As travel frequently occurs across borders – 45% of nights booked on Airbnb over 2023 were cross-border (ie. where the country of the guest differed from the location of the property booked) – ABNB’s and BKNG’s networks are truly global networks. This has meant that any local competitor of ABNB or BKNG has had a very difficult time competing with these two juggernauts, as the smallest network that would enable a competitor to compete is extremely large and spans entire countries, rather than cities – and this doesn’t even consider the gushes of cash being produced by ABNB and BKNG that can be reinvested back into improving their product, which again makes the prospect of a start-up or other competitor taking market share from these incumbents all the more unlikely. Consequently, the barriers to entry in running a successful and profitable OTA are incredibly high. We estimate the cost of replicating ABNB’s and BKNG’s leading positions in their respective markets greatly exceeds their current market capitalisation – a would-be competitor would likely be better off buying shares in ABNB and BKNG rather than trying to compete!

Even though Airbnb is the youngest in the OTA industry, it has made a significant impact on the way guests book accommodation globally. Through an easy-to-use platform, Airbnb has enabled Hosts with underutilised homes to earn incomes by renting out to the myriad of Guests looking for a cheaper and better alternative to hotels, particularly relating to group trips (which make up the majority of bookings on the platform).

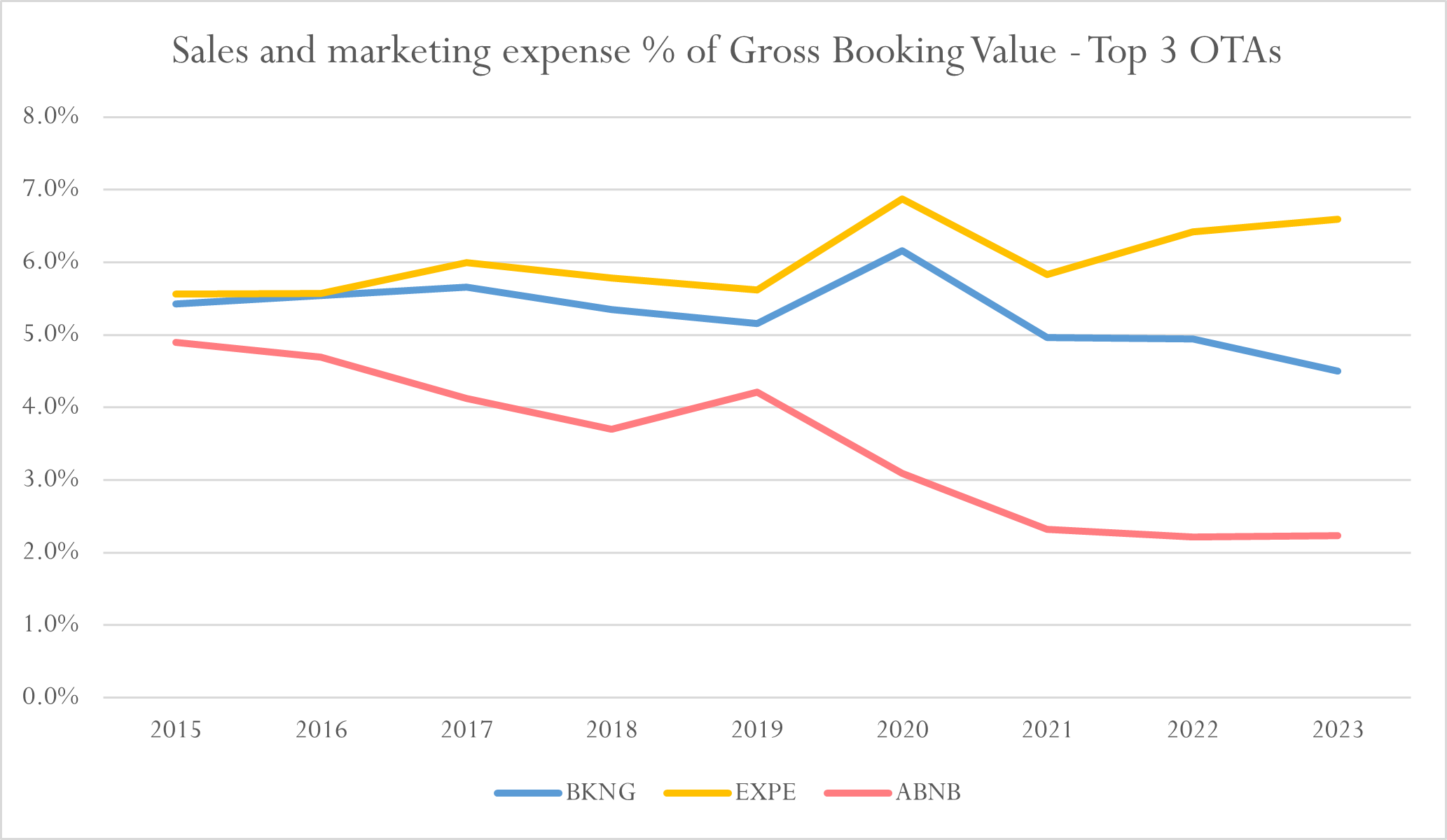

Airbnb is the most differentiated of the major OTAs with the most unique supply of accommodation, which seems to have led to their profit margins being higher and performance marketing expenditures being lower with respect to GBV when compared to BKNG and EXPE, who have far more overlap in the supply-side of their marketplaces.

Sources: Airbnb (ABNB.NAS), Booking Holdings (BKNG.NAS), and Expedia (EXPE.NAS) 10K filings.

We estimate that over 80% of Airbnb’s listings are unique to Airbnb, meaning if Guests want access to the long tail of unique homes and stays, they have to come to Airbnb. Additionally, a majority of these listings are also by individual or non-professional Hosts who – without Airbnb’s merchant facility, large user base of potential Guests and extensive profiles to build trust – wouldn’t have the capabilities to individually monetise their under-utilised homes. This differs to BKNG and EXPE’s supply which is largely comprised of large hotel chains and professional hosts who have entire marketing teams and budgets to manage the various channels they may acquire new guests from and improve occupancy rates. Additionally, over 90% of Airbnb’s bookings are made via direct channels, showing strong customer loyalty and that Airbnb is a primary search destination for many accommodation bookers globally.

While ABNB is the most differentiated of the major OTAs, they’re increasingly crossing swords with BKNG who is pushing further into ‘alternative accommodation’ (non-hotel short-term accommodation) while ABNB expands slowly into hotels. Despite this, it’s hard to see the competitive intensity between these two businesses ever being overly aggressive. Both management teams have committed to returning significant amounts of capital to shareholders on an ongoing basis and are aware of the significant barriers to entry that protect them against insurgents.

The greenfield opportunity is also still quite significant with ABNB focusing more on acquiring longer term stay demand through Airbnb-friendly apartments and other unique supply rather than hotels, and BKNG focusing on professional supply of alternative accommodation (who often leverage costly channel management software solutions such as Siteminder to cross-list their homes on multiple booking platforms including ABNB and BKNG) rather than individuals, so the cross over may continue to be quite limited over the medium term. ABNB’s continued focus on improving the consistency and quality of short-term accommodation listings on their marketplace should also enable them to continue to take share from the hotel industry, representing an immense available opportunity given nights spent in hotels currently exceed nine for every one night spent in an Airbnb.

As an aside, the more commoditised nature of BKNG’s marketplace supply also makes it more vulnerable to the increasing popularity of Google Hotels – a meta-search engine that crawls hotel prices and availabilities across both hotel websites (ie. Marriott, Hilton, Premier Inn, etc.) and OTA websites (Booking.com, Agoda.com, Expedia.com, Hotels.com, wotif.com, etc.) to allow Guests to better compare their hotel options – than ABNB. However, BKNG’s increasing investments in the Genius Loyalty program and the mobile app experience has made them less reliant on Google for growing booking volumes over time.

The concentrated nature of the OTA market, dominated by ABNB, BKNG and EXPE, coupled with their focus on shareholder returns and profitability, makes significant increases in competitive rivalry unlikely in our view. This oligopolistic structure, with its high barriers to entry, is quite conducive to attractive long-term shareholder returns and stands in stark contrast to the 'bloody ocean' present in the commoditized areas of the value-chain, such as consumer-to-business (C2B) payments and point-solution software, where numerous competitors fight for marginal returns. While there may be some continued competitive pressures from the likes of Google, we believe that competition within the OTA industry is more likely to remain relatively benign over the longer-term, akin to successful duopolies like Visa and Mastercard, than to go the way of the pay-fac and merchant services industries.

Pleasingly, Airbnb’s co-founder and CEO, Brian Chesky, still leads the business today, and despite his personal stake in the business being worth a tidy US$11 billion, he seems as passionate and hungry about Airbnb’s mission as ever. It’s quite rare to see such a high-quality business paired with a driven and talented management team, however that’s exactly what we have with ABNB. Brian Chesky is very close to the engine room of the business and is often talking to customers as well as being involved in the final signoffs of major product updates, despite heading up an organisation of nearly 7,000 employees.

Additionally, Brian Chesky has one of the most truly long-term incentive packages we’ve ever seen with the final tranche of his ‘Multi-Year Award’ vesting in November 2030, 6.4 years from today and 10 years from the initial grant. With an average annual share price increase of 20% from today (a 3.1x multiple on today’s share price) required for him to receive the bulk of his LTI, there is absolutely no room for complacency, and we look forward to Brian’s continued focus on efficiency, innovation, and improving value for both sides of their dominant marketplace delivering attractive returns for us as shareholders over the long-term.

While ABNB has cemented an enviable position for itself in their leading markets of the US, UK, Australia and Canada, they still have a large opportunity to grow bookings globally in under-penetrated regions of APAC and Europe. Given the cross-border network effects inherent in their leading marketplace, we’re confident that their success in their existing markets will be transferable to newer markets.

At our cost base, ABNB was valued at ~23x current free cash flows (FCF). We view this as an undemanding price to pay for a business as high a quality with a management team as aligned and focused on the long-term, yet with an attractive growth opportunity that will require no further incremental capital investments in the business. With an impregnable balance sheet, very high barriers to entry, and significant cash generation, the risk of permanent capital loss in holding Airbnb’s shares is very low.

While there is no single ‘catalyst’ that will see us quickly earn a return on our recent share purchases we expect to earn a predictable, yet meaningful, risk-adjusted return on our capital invested in this high-quality business exceeding our 10% p.a. Benchmark as the company continues to increase its global penetration, free cash flows, and share repurchases over the next 5-10 years.

Now, back to the ASX microcaps…

BM.

Disclaimer: This document contains general information only and is not an investment recommendation. Blue Stamp Company Pty Ltd (ACN 141 440 931) (AFSL 495417) (‘Blue Stamp’) is the Trustee and Manager of the Blue Stamp Trust (‘Trust’). Blue Stamp accepts no liability for any inaccurate, incomplete or omitted information of any kind or any losses caused by using this information. Blue Stamp does not guarantee the performance or repayment of capital from the Trust. Past performance is not a reliable indicator of future performance. Please consider the Information Memorandum (‘IM’) and investment risks before making any decision to invest, acquire or continue to hold units in the Trust.